Strategic planning is an important and necessary process for businesses of all sizes. It provides many benefits that can greatly improve the success of a business, as well as its continuity over time. This article will discuss the various advantages associated with strategic planning, such as increased efficiency and better decision-making capabilities. Additionally, this paper will explore how effective implementation of a strategic plan can lead to improved financial performance and greater customer satisfaction. By understanding the importance of strategic planning and its specific benefits, organizations can be better equipped to make informed decisions regarding their future growth and development.

Effective strategic planning requires a deep analysis of both internal and external factors that are likely to influence the organization’s operations in the short or long term. Strategic plans must take into account elements like market trends, competitive landscape, organizational goals, available resources, and potential risks. These considerations provide insight into what direction an organization should pursue in order to maximize profit margins while minimizing any negative impacts on customer relations or operational costs. A comprehensive approach to strategic planning is essential for maintaining successful operations on a continuous basis.

The ultimate goal of any strategic plan is to create value for stakeholders through the efficient use of resources. An appropriate strategy involves finding a balance between cost control measures and investments in innovative products or services that could potentially generate higher returns on investment (ROI). Through proper evaluation of current conditions, realistic objectives can be set that serve as guideposts along the way toward achieving desired outcomes in terms of profitability and other key performance indicators (KPIs). In this respect, having an actionable plan helps organizations stay focused on their core mission while adapting quickly to changes within the industry landscape.

Definition

“A stitch in time saves nine,” is an adage that emphasizes the importance of taking action and planning ahead. Strategic Planning is a process by which organizations set forth their desired direction, allocate resources to support it, and evaluate progress toward reaching stated goals and objectives. In other words, strategic planning can be defined as the process of setting specific long-term organizational goals with short-term strategies for achieving them. The purpose of this type of planning is to ensure that all components of an organization are working together to meet established objectives.

The basic steps involved in the process include assessing current situations, identifying opportunities for growth or improvement, developing plans and strategies to reach those goals, implementing plans, managing change, monitoring performance over time, and making necessary adjustments. A successful strategic plan requires careful consideration of multiple factors including financial resources, human capital, and operational capacity among others. Each component must work together harmoniously for success; otherwise, the entire effort may fail.

In order to effectively manage any organization’s future course of action and minimize the risk inherent in decision-making processes, it is essential to have a well-defined strategy created through comprehensive research and analysis followed by clear communication throughout an organization’s chain of command so that everyone understands what needs to be achieved at every level. With this approach comes improved clarity on how best to achieve organizational targets while also providing greater accountability amongst stakeholders – increasing chances of success overall. Moving onto the next section about ‘goals and objectives’, we will look further into how these elements come together when creating effective strategic plans.

Goals And Objectives

Goals and objectives are key components of the planning process, as they provide direction to an organization’s strategic vision. Goals should be specific and measurable, while objectives should focus on how goals will be achieved over time. In other words, goals create a long-term path for progress whereas objectives are smaller steps that must be taken in order to reach those goals. It is important to remember that achieving organizational success requires dedication from all levels within an organization and clear communication about what needs to be done when it comes to setting achievable targets.

The development of effective goals and objectives can help bring structure and purpose to any strategic plan by providing members of an organization with clearly defined expectations for performance. A well-crafted goal or objective should have four main components: (1) a timeline; (2) an actionable item; (3) measurable outcomes; and (4) desired results. By combining these elements together, organizations can develop strategies that ensure everyone involved knows exactly what tasks need to be completed, how long each task is expected to take, as well as what kind of outcome is required at the end of the project cycle.

In addition, having regularly scheduled reviews of progress against established goals and objectives allows decision-makers within an organization to accurately evaluate the efficacy of their plans in real-time – enabling them to adjust course based on feedback received or unforeseen circumstances encountered along the way. This systematic approach enables organizations to remain agile enough to adapt quickly whilst still ensuring resources are used efficiently towards reaching pre-determined targets. Moving onto the next section we will explore further into this concept by looking at the ‘systematic process’.

Systematic Process

A systematic process is a critical component for any organization looking to successfully execute its strategic objectives. It ensures that the most effective approach is taken in achieving those goals, maximizing efficiency, and minimizing waste. When it comes to implementing an effective strategy, this step-by-step process should include:

- Process Improvement – Identifying areas of improvement within existing systems and processes as well as developing new ones where necessary;

- Strategic Implementation – Formulating actionable plans based upon identified improvements and ensuring they are put into practice;

- Monitoring & Evaluation – Constantly evaluating progress against established targets and making adjustments accordingly if needed;

- Risk Management– Developing contingency plans to address potential risks associated with each stage of the implementation process. By following these steps, organizations can ensure that their strategies will be implemented in a manner that optimizes resources while still allowing enough flexibility to adapt quickly when circumstances change or unexpected events arise. The next section will focus further on how risk management plays an important role in successful strategy execution.

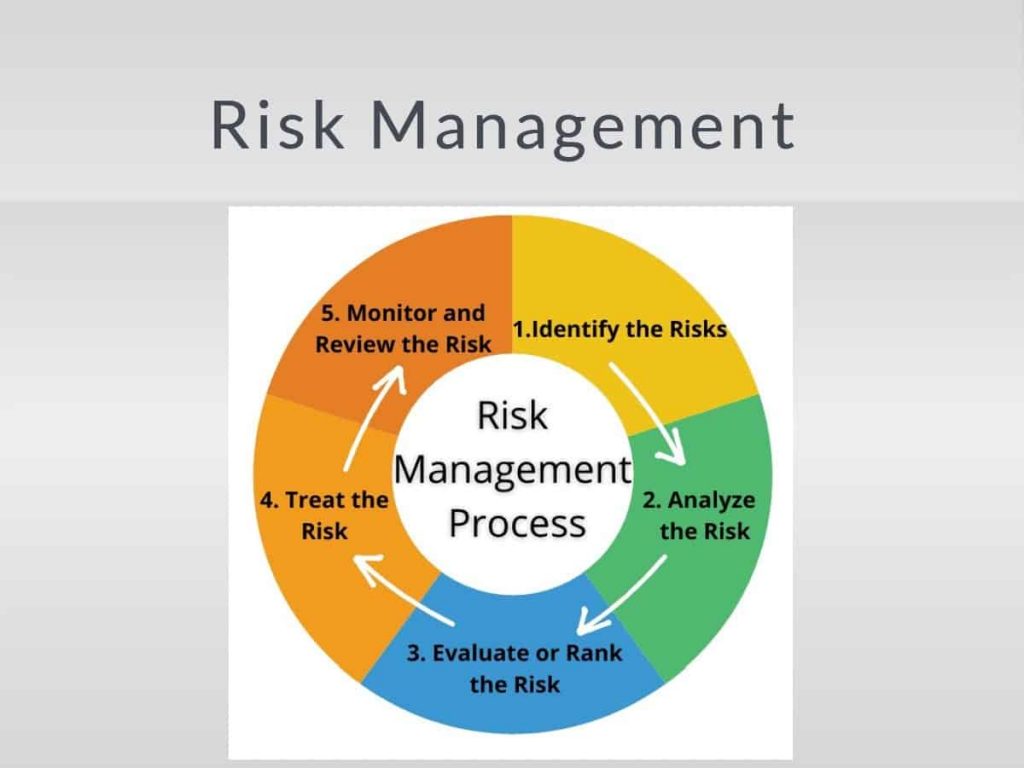

Risk Management

Risk management is an essential factor in the successful implementation of any strategic plan. Strategic risk can be defined as “the inherent uncertainty in achieving a desired outcome due to external and internal factors” (Gandz, 2010). To effectively manage risks associated with strategy execution, organizations must first undertake a thorough analysis and assessment of all potential risks. This requires identifying key areas of vulnerability that may lead to disruption or failure, understanding their likelihood of occurrence, and evaluating their impact on the organization’s objectives.

Once identified, appropriate mitigation strategies should be developed which outline how each risk will be addressed. Strategies such as diversification, cost containment measures, and alternative planning options provide ways for organizations to minimize losses if faced with adverse circumstances. Additionally, monitoring systems should also be put into place so that any changes in the environment can be quickly detected and corrective action is taken where necessary.

Resource allocation plays an important role when it comes to mitigating risks associated with strategy execution. Without proper budgeting and personnel resources allocated toward managing these issues, businesses are more likely to experience negative impacts which could have been avoided through proactive preparation. Therefore, careful consideration needs to be given when determining resource requirements for strategic risk management initiatives.

Resource Allocation

Resource allocation is an essential part of any strategic planning process. By taking a comprehensive approach to budgeting, resource planning, workforce planning, and financial management, organizations can ensure that their strategies are properly implemented in order to achieve desired outcomes. Budgeting involves allocating funds for various activities related to the strategy execution such as research & development, marketing expenses or operational costs. Resource planning seeks to identify the necessary resources needed for each activity based on the goals set out by the strategic plan. Workforce planning helps organizations secure necessary personnel while ensuring they have sufficient skills and experience required to execute tasks efficiently. Finally, cost control measures should be put in place so that unnecessary expenditure is avoided and only appropriate investments are made when needed.

Through effective resource allocation, organizations will gain greater certainty about their ability to carry out the objectives outlined in their strategic plans. Furthermore, it also ensures that there is enough flexibility available within the organization’s budget which allows them to take advantage of opportunities as they arise without having to rely solely on external sources of funding. With careful consideration given to how best to allocate resources across different areas of operations, businesses can make sure that their strategies remain viable even amidst changing market conditions.

Communication Strategies

An integral component of any strategic plan is an effective communication strategy. Effective communication can ensure that stakeholders are kept informed and engaged, while also allowing team members to stay aligned throughout the planning process. Communication strategies should be tailored to meet the specific needs of the organization and its stakeholders; this includes both internal and external communications such as public relations activities, media outreach, or customer service initiatives.

In order to implement a successful communication strategy, organizations must first develop a comprehensive communication plan which outlines objectives, roles & responsibilities, and target audiences for each message. It is also important for companies to make sure that their messages resonate with their audience by considering language style and tone when crafting content. Additionally, businesses should consider the various channels available for delivering information in order to reach their intended audience effectively.

To summarise:

• Establishing a detailed communication plan is essential for creating an effective communication strategy.

• Tailor communications to suit different types of stakeholders based on their individual needs.

• Consider language style and tone when crafting content in order to create meaningful connections with your audience. These steps will help organizations achieve clarity around key messages so they can communicate them effectively throughout all stages of the strategic planning process. By taking these steps into account, organizations can increase stakeholder engagement while ensuring team alignment across departments and functions. This facilitates decision-making processes within the organization as well as allows leaders to remain agile when addressing changes in market conditions.

Decision Making

Decision-making is an essential part of any strategic planning process. According to a recent survey, 80% of business leaders believe that having a sound decision-making process in place is critical for successful strategy execution. When it comes to decision-making, there are several steps involved:

• Problem Identification and Analysis: Companies must identify the problem they are trying to solve and then analyze the data available so they can make informed decisions. This includes gathering relevant information from stakeholders, conducting research on industry trends, and analyzing customer feedback.

• Plan Creation: After identifying and analyzing the problem at hand, companies must create a plan based on their analysis which outlines specific objectives and strategies for achieving them. This will help ensure that all team members remain aligned throughout the planning process.

• Strategy Building: Once a plan has been created, organizations should develop detailed strategies for reaching the goals outlined in the plan. This requires careful consideration of factors such as resources required (time & money) as well as potential risks associated with different approaches.

• Data Analysis: As plans are implemented, businesses must continue to monitor progress using key performance indicators (KPIs). Regularly tracking KPIs allows organizations to measure the success or failure of strategies quickly so adjustments can be made if necessary.

These four steps form the foundation of effective decision-making processes within an organization; when executed properly these processes allow companies to successfully navigate changes in market conditions while remaining agile enough to adjust their strategic plans accordingly.

Adaptability To Change

Adaptability to change is an essential component of any successful strategic plan. Companies must be able to quickly and effectively adapt their plans in order to stay ahead of competitors and remain competitive in the market. In order to do this, businesses need a comprehensive change management system that will help them anticipate potential changes in the market and adjust their strategies accordingly.

Change management systems can involve elements such as scenario planning which helps organizations identify possible future scenarios for the business environment. This allows companies to develop several different strategies simultaneously so they are prepared for various outcomes. Additionally, it’s important for companies to have measures in place to assess their “change readiness”; these measures can include evaluating internal capabilities, assessing external resources, and considering financial implications when making strategic shifts.

By taking proactive steps towards adapting to changing conditions, companies can ensure that they are well-positioned no matter what happens within their industry or the global economy. Moreover, having a flexible strategy in place gives organizations an advantage over those who only react after changes occur instead of preparing beforehand. Moving forward with these considerations will allow businesses to benefit from improved performance both now and into the future.

Improved Performance

Utilizing strategic planning to ensure improved performance is a key factor in ensuring long-term success. Once the initial plan has been determined, businesses need to track performance and make adjustments as needed in order to stay on target. This involves staying abreast of market trends, customer needs, and competitors’ strategies so that any potential changes can be addressed quickly. Additionally, regular meetings should be held with team members responsible for implementing the strategy in order to keep everyone informed about the progress made toward goals.

Additionally, it’s important for companies to develop an effective decision-making process when making strategic decisions regarding their plans. This includes involving all stakeholders such as employees and customers in order to gain valuable input from different perspectives which will help inform more comprehensive strategies. Furthermore, setting clear objectives helps give direction while also allowing managers to measure and evaluate progress against measurable metrics. Doing this allows organizations to identify areas where improvement may be necessary or not meeting expectations.

Having a good understanding of what drives business performance enables executives to make better strategic decisions that are aligned with longer-term goals such as profitability and growth targets. With the right data at their disposal and appropriate processes in place, businesses can use their insights effectively in order to reach desired outcomes over time and increase competitive advantage within their respective markets. Moving forward with these considerations will help ensure long-term success for many organizations.

Long-Term Success

Having a comprehensive strategic plan in place is essential for long-term success. It provides the necessary framework to create and maintain a clear vision of what goals are desired, how they can be achieved, and when they should be met. This requires critical thinking skills coupled with task organization in order to craft an effective strategy that will bring about the best possible outcomes over time.

The key components for achieving long-term success include:

- Developing a Strategic Vision: A company needs to identify its purpose and objectives before any planning can take place. This includes analyzing current conditions as well as looking into future trends so that potential opportunities or risks can be identified more easily. Doing this helps ensure that all decisions made along the way align with the overall mission and values of the organization.

- Future Planning: Once a broad vision has been established, it’s important to think ahead about where the business wants to go next and how different strategies could help get them there. This involves taking into account potential external factors such as market changes or competition which may have an effect on operations down the line. Additionally, longer-term goals need to be set in order to provide direction while also allowing room for flexibility if needed in case of unexpected developments arise.

- Critical Thinking & Task Organization: Having good problem-solving abilities combined with strong organizational skills allows executives to make informed decisions based on data rather than gut feeling alone. This means having access to accurate information regarding performance metrics as well as being able to effectively delegate tasks among team members so everyone knows who is responsible for what at all times. Doing this ensures that each individual involved understands their role within the bigger picture and contributes towards meeting predetermined targets quickly and efficiently.

With these considerations taken into account, companies are better equipped to achieve their desired results through careful strategizing and efficient execution over time – thereby ensuring long-term success regardless of industry or size of operation.

Frequently Asked Questions

When it comes to implementing a strategic plan, there is often confusion around the timeline. Many business owners may think that creating and executing a strategy will be done in one day or even overnight when this simply isn’t true. Despite this misconception, understanding the timeline for implementing a strategic plan is essential as it provides clarity on what needs to be accomplished and how long each step should take.

Firstly, defining objectives is an important initial part of developing a successful strategy. This process can involve researching customer requirements and expectations and setting goals accordingly which can take anywhere from two weeks to three months depending on the size of the project. Once objectives are set, then comes drafting strategies which involve brainstorming ideas with stakeholders and exploring possible solutions. This stage usually takes four weeks but can last up to eight if dealing with more complex projects. Afterward, tactics need to be developed where detailed action plans are devised such as deciding who will carry out each task, allocating resources, assigning roles, etc., this typically requires another month or two before implementation begins.

Accountants would advise that businesses factor in plenty of time for testing new strategies before fully committing – at least six months so any potential issues can be identified early on. It’s also wise to forecast future changes by incorporating flexibility into your overall plan which allows you to adjust quickly if needed. Additionally, regular reviews are necessary during the entire process as they help document progress, ensure accountability, and identify areas that require further improvement along the way.

In summary, although implementing a strategic plan does not happen overnight as many assume; understanding its timeline helps provide clarity on what needs to be accomplished and how long each step should take ensuring success in reaching desired outcomes.

Strategic planning is an essential component of effective business management. It involves long-term planning for organizational goals and objectives, helping businesses to create a competitive advantage in the marketplace. A well-structured strategic plan can help ensure the success of any organization by providing greater clarity and focus on future initiatives.

When developing a comprehensive strategic plan, there are several key steps that must be taken. Firstly, it is important to clearly define the mission and vision of the company; what will be achieved over time, and how this aligns with both short-term and long-term objectives. Then, specific strategies should be established which outline how these goals can be met such as implementation timelines and resources required. Finally, regular assessment of progress should take place so that adjustments can be made if necessary.

By engaging in proactive strategic planning, businesses are able to anticipate changing market trends more effectively while setting realistic expectations for results. This helps organizations remain agile when responding to external factors like customer demand or industry competition. Furthermore, having a detailed understanding of potential risks also provides businesses with peace of mind that their operations are running smoothly and efficiently.

Benefits include:

• Improved decision-making processes through analysis of data

• Enhanced productivity from increased workforce efficiency

• Development of sustainable competitive advantage through fostering innovation

• Improved customer satisfaction through timely and accurate service

The current H2 question asks: What are the most common obstacles to successful strategic planning? In order to answer this, it is important to understand what constitutes a barrier and how these barriers can be addressed through the successful implementation of organizational goals.

Barriers may include inadequate resource allocation, conflicting objectives between departments, or team dynamics that hinder progress toward achieving those objectives. Resource allocation issues can arise when there is not enough funding available for an organization to implement its strategy, or when resources are misallocated due to poor planning processes or a lack of understanding about the importance of each task in meeting long-term goals. Conflicting objectives occur when different departments within an organization have different ideas about how best to achieve their individual goals and do not come together on a unified vision. Finally, team dynamics can also create hurdles by creating tension among members who cannot agree on tactics or approaches.

In order to successfully overcome these obstacles, it is important for organizations to evaluate their existing strategies and adjust as needed based on market trends and other external factors. Additionally, they must ensure proper training is provided so all employees understand the overall mission and purpose behind any new initiatives being implemented. Furthermore, effective communication amongst all levels within an organization should be established in order to foster collaboration and innovation which will ultimately lead to more successful outcomes in terms of reaching desired results.

By assessing potential impediments upfront and proactively addressing them with well-thought-out plans and clear expectations, organizations can better position themselves for success in executing their strategies going forward.

The size of an organization plays a critical role in the process of strategic planning. When it comes to organizational size, smaller organizations typically have fewer resources and fewer personnel compared to larger organizations. This means that they must focus their attention on specific areas in order to remain competitive while achieving success with their plan.

Larger organizations, however, can benefit from having more financial and human capital at their disposal when developing a strategic plan. With additional resources available, larger companies are able to assign responsibilities across multiple departments and create powerful plans that cover all aspects of operations. They may also be able to allocate budgets for training staff or other activities needed for implementation within shorter timelines than smaller businesses often require.

In either case, effective use of available resources is key for successful strategic planning regardless of the size of the company. If a business is able to identify its strengths and weaknesses as well as opportunities and threats in order to develop a comprehensive strategy tailored around these factors, then it stands a better chance of gaining a competitive advantage over its competitors. Ultimately, proper utilization of organizational size during the development phase helps ensure success with the subsequent implementation timeline once the plan has been finalized.

Strategic planning is an important business activity that enables organizations to set goals, allocate resources and develop action plans. It also helps organizations identify potential risks and plan measures to mitigate them. As a result, the success of any strategic plan depends on its contents. This article discusses what should be included in a strategic plan in order to ensure its efficacy.

To begin with, it is essential for organizations to define their strategic objectives when developing a strategic plan. These objectives serve as guiding principles for setting future goals and evaluating performance over time. Additionally, goal-setting plays a crucial role in strategic planning by helping organizations determine which tasks are necessary for achieving desired outcomes within specified timelines. Moreover, resource allocation is another vital component of successful strategic planning; it ensures that all organizational activities are adequately funded and managed effectively.

Furthermore, creating an effective action plan requires careful consideration of various factors such as available resources, target audience, and projected results. An action plan must include detailed steps outlining how each goal will be achieved along with measurable milestones which can track progress over time. Lastly, risk management forms an integral part of any strategic plan since it allows organizations to anticipate potential threats and prepare accordingly so they can quickly respond if needed.

In summary, defining clear objectives, setting achievable goals, allocating adequate resources, and developing well-structured action plans are key components of a successful strategic plan while assessing possible risks provides additional security against unexpected events or challenges.

Conclusion

A strategic plan is essential for any organization to achieve its desired goals. It serves as a roadmap that allows organizations to take the necessary steps in order to reach their objectives. While developing and implementing a successful strategic plan may seem daunting, it can have many benefits for an organization.

The first benefit of having a comprehensive strategic plan is creating a competitive advantage. Organizations are able to identify potential opportunities and capitalize on them before competitors do, thus allowing them to gain market share over time. Additionally, by understanding customer needs better than other companies, they can create products or services tailored specifically to those customers which will help increase sales and brand awareness.

Organizations must also consider common obstacles when planning strategically; these include a lack of resources, failure to recognize external threats, and inefficient communication between departments. In addition, the size of an organization can affect how much time and effort should be put into the process. Smaller organizations need more detailed plans since they have fewer resources available while larger organizations require shorter-term plans due to their greater ability to respond quickly to changes in the environment.

To ensure success in executing a strategic plan, certain components such as clear objectives, measurable KPIs (key performance indicators), resource allocation plans, risk management processes, and contingency plans should all be included. Ultimately though, who is responsible for ensuring that each component has been addressed? How can organizations guarantee that their efforts will pay off once the plan has been implemented?